A weekly look at the trends driving economies and investments worldwide.

Full release now available below

Fed’s Hawkish Cut: The Fed delivered a 25bp rate cut, but Chair Powell’s hawkish tone challenged market bets on rapid easing. He stressed that a December cut is “far from assured”, pushing front-end yields higher.

QT Ends, Yields Rise: The Fed announced an end to quantitative tightening for Treasuries, with MBS reinvestments redirected into T-bills. Despite this balance-sheet shift, longer-term yields rose, reflecting Powell’s caution and dissent within the FOMC.

ECB Holds Steady: The ECB, ,meanwhile, kept its deposit rate unchanged at 2%, as expected.

President Lagarde noted that downside growth risks have eased, pointing to improving global conditions, but offered little new guidance. The Bank reiterated its data-dependent stance, and markets now see no rate moves through 2026.

Insights

This chart illustrates the relationship between 2 and 10-year US Treasury yields alongside the Fed Funds Target Rate.

As the Fed began cutting rates, we initially saw a bear-steepening but, a market friendly bull steepening emerged after the 3rd cut.

While the impact of the latest cuts remains uncertain, there is growing doubt about the Fed’s ability to meaningfully improve the current low hiring and low firing environment despite prioritising the labour market over persistent inflation.

Recent signs of weakening unemployment, combined with ongoing trade frictions and trade pressures, add further uncertainty to the outlook.

Insights

The reaction of UST yields to the last three Fed rate cuts highlights a clear divergence along the curve.

Short-term yields, such as the 3-month and 2-year, fell or moved only modestly, reflecting the direct impact of lower policy rates and expectations of further easing.

In contrast, longer-term yields, notably the 10-year and 30-year, rose, signaling that investors anticipate stronger growth and persistent inflation.

Following the hawkish rate cut on October 29 and the conclusion of quantitative tightening, it will be interesting to observe how the yield curve evolves, with expectations pointing to a broad-based rise in yields and a steepening of the curve.

Insights

This chart showcases how the DXY has moved 252 observations before and 252 after each of the last five Fed rate cuts.

The response of the DXY to the past five cuts highlights a general upward short-term shift in the first 50–100 days after each cut, followed by a gradual decline in the index into negative territory.

This pattern suggests that, while the dollar may show brief resilience immediately after a policy move, it typically weakens as markets adjust to a sustained easing cycle and narrowing rate differentials.

Insights

Alongside the rate decision, the Fed announced an end to quantitative tightening (QT) for US Treasuries and will begin reinvesting all maturing principal payments into T-bills starting December 1.

This effectively marks the end of balance sheet reduction — a major shift in liquidity dynamics.

The move aims to stabilise reserve balances and ease upward pressure in short-term funding markets, which have recently shown signs of strain.

Insights

Despite the balance-sheet pivot, long-end yields moved higher, reflecting a market view that the Fed’s hawkish tone outweighs the liquidity injection.

Dissent within the FOMC — including calls for a larger cut — underscores growing debate about how quickly the Fed should ease policy.

Explore this week’s Macro Trends insights from Macrobond with the second installment below.

With inflation easing and growth momentum fading, the ECB faces renewed pressure to support the eurozone economy.

Markets are divided on whether policymakers will signal another rate cut before year-end.

Insights

Market pricing across EURIBOR futures, OIS, and €STR futures suggests that investors expect the ECB to remain on hold for an extended period.

Following the sharp hiking cycle that peaked in 2023, the implied rates indicate only limited easing priced in for 2025, with a broadly stable path thereafter. This aligns with the broader consensus that the ECB will pause before considering gradual rate cuts, as inflation continues to moderate but remains above target.

Insights

Market expectations for the end point of the easing cycle have shifted unevenly across major central banks.

The Fed and BoE terminal rates have both moved lower, indicating that investor snow expect deeper rate cuts in the US and UK. In contrast, the ECB’s terminal rate has edged higher, suggesting markets anticipate a more limited easing path in the euro area.

Insights

All four key components of the Euro Area PMI are now above the 50 threshold, signalling a return to expansion. Production (52.2)and new orders (51.9) point to improving activity and stronger demand, while employment (50.8) indicates modest job growth.

Meanwhile, output prices (52.8) suggest that price pressures persist, though at a manageable pace. Overall, the data support the view of a gradual recovery in the Euro Area economy.

Insights

The ECB’s September projections show slightly higher inflation in the near term compared with June, reflecting persistent price pressures.

However, the longer-term outlook was revised lower, with inflation now expected to fall below 2% — suggesting the ECB sees disinflation continuing toward its target over the coming years.

This gives the central bank greater room to shift its focus toward supporting growth in the euro area rather than containing inflation.

Insights

The French political fall has been eventful with François Bayrou and Sébastien Lecornu, the latter being re-appointed on 10 October. In total it’s six prime ministers since May 2022,the two prior to Lecornu lost no-confidence votes over their budget plans, a factor cited by Fitch Ratings in its recent sovereign rating downgrade.

Markets responded early: both the OAT-Bund 10-year spread and France 5-year CDS began rising ahead of the shake-ups. That suggests investors were already pricing in heightened political and fiscal uncertainty before the official reshuffles.

Explore this week’s Macro Trends insights from Macrobond with the first installment below.

The US government remains in shutdown, leaving markets with very limited access to official economic data. Still, there is broad expectation that the Fed will move ahead with a rate cut this week:

Markets brace for a Fed rate cut as the US data blackout leaves investors searching for signals.

Insights:

Markets are fully pricing a 25 bp rate cut, with attention shifting to forward guidance rather than the decision itself.

The Fed’s dot plot still signals a gradual easing path, while Fed funds futures expect a faster decline toward ~3% by 2026. That divergence will drive the market reaction.

Insights:

Stephen Miran was sworn in as a member of the Federal Reserve Board of Governors on September 16, 2025.

With Miran joining the FOMC, the dot plot took on a new shape — as he stood out as the only member projecting a Fed funds rate below 3%, signaling significant cuts.

The new Fed governor will likely attract extra attention, especially as discussions around Powell’s eventual successor gain momentum.

Insights:

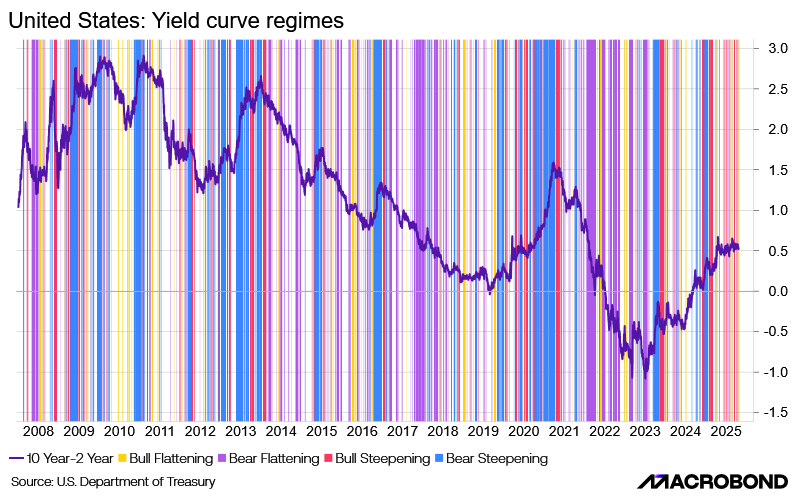

The Federal Reserve is in a rate-cutting cycle, while Trump’s fiscal policies are pushing longer-term yields higher through expectations of larger deficits and increased Treasury issuance. This mix of monetary easing and fiscal expansion is steepening the yield curve.

A key debate now is whether the steepening will be bearish or bullish:

Insights:

The direction this steepening takes will be crucial for market positioning, as equity valuations and fixed-income returns tend to react very differently under bear versus bull steepening regimes.

In this chart, you can see the historical performance of various equity sectors, fixed income, and gold across these different yield-curve environments.

Insights

With the U.S. government shutdown halting operations at the Bureau of Labor Statistics (BLS), official labor market data — including the monthly Nonfarm Payrolls report — will not be released. This data blackout leaves policymakers and markets without one of their most important economic indicators. In the absence of BLS data, attention will turn to ADP’s private-sector employment report as a key alternative gauge of labor market momentum ahead of the Fed’s upcoming policy decisions.

Insights

Last Friday, despite the ongoing government shutdown, markets received fresh economic data — the Consumer Price Index (CPI) for September.

The report showed that inflation remains stubbornly high at 3 percent, reinforcing concerns that price pressures are proving more persistent than the Federal Reserve had hoped.

This resilience in inflation is likely to weigh on the Fed’s upcoming policy discussions, as it complicates the path toward potential rate cuts and raises questions about how long restrictive monetary conditions will need to stay in place.