A bi-weekly look at the trends driving economies and investments worldwide.

Energy markets remain the clearest transmission channel: Tensions around Iran have lifted oil and LNG risk premia, highlighting the sensitivity of Gulf shipping routes and amplifying volatility across global energy markets.

Inflation risks are returning through the energy channel: Higher energy costs risk stalling disinflation, with Europe more exposed through import dependence while the United States remains partly buffered by domestic supply.

Policy expectations are adjusting as markets reassess the outlook: Rising energy prices have prompted markets to retrace easing expectations, as investors reassess inflation risks and the potential path of policy across major economies. A stronger dollar typically pressures EM duration, while higher energy costs tend to rotate equities toward defensive sectors and larger companies.

Insights

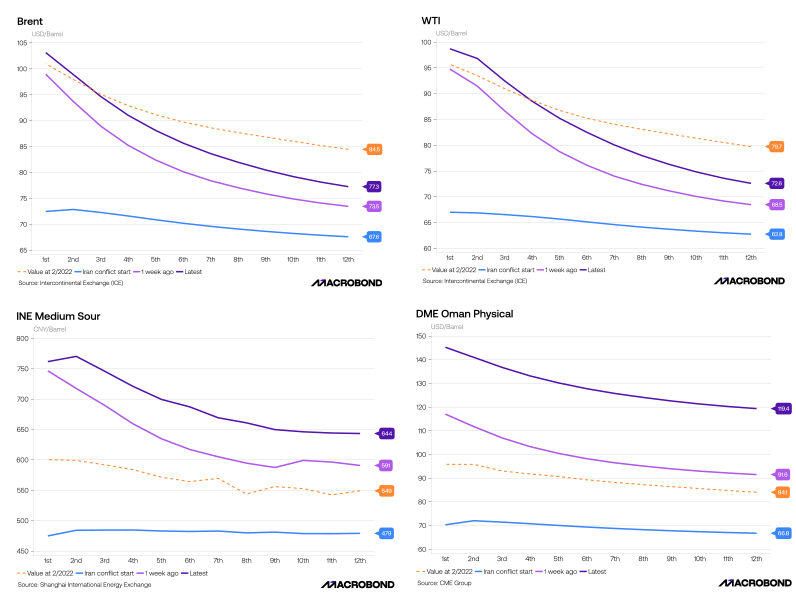

Energy markets are responding unevenly to renewed Middle East tensions, reflecting regional exposure to supply risks. European benchmarks have reacted sharply, consistent with the region’s structural dependence on imported energy. U.S. markets have also moved given their role in global pricing, though strong domestic production provides partial insulation. Regional Middle Eastern grades appear particularly sensitive as risks center on nearby supply routes — evident in the current reaction compared with past geopolitical events outside the region.

Meanwhile, reports suggest vessels linked to Chinese trade have been among those allowed to transit the Strait of Hormuz despite broader shipping disruptions, potentially cushioning Chinese crude markets.

Insights

The Strait of Hormuz remains the most important energy chokepoint globally. Roughly one-fifth of global oil consumption and a similar share of LNG trade passes through the narrow passage each day, linking Gulf producers to international markets. The strait sits next to the North Dome / South Pars complex, the world’s largest natural gas field shared by Qatar and Iran.

Most flows are destined for Asian markets, though Europe remains exposed through LNG pricing and global gas linkages. As geopolitical tensions rise, even partial disruptions to traffic through Hormuz can quickly tighten global supply, amplifying volatility in both oil and natural gas prices.

Insights

European gas storage levels are currently well below typical seasonal levels, implying a larger-than-usual refill requirement ahead of next winter. At the same time, escalating tensions in the Middle East have lifted energy risk premia, reinforcing concerns about LNG supply and leaving sentiment in European gas markets cautious.

Insights

Escalating tensions in the Middle East have lifted energy risk premia, raising the risk that the disinflation trend stalls. Europe is typically more sensitive toenergy shocks due to its reliance on imported fuel. Conversely, the U.S. enters this phase with inflation already running relatively higher, supported by resilient domestic demand.

As a result, Europe could see a sharper near-term acceleration in inflation and, if the energy shock persists, headline inflation across Europe could rise above U.S. levels despite starting from a lower base.

Insights

The Fed has been able to ease despite inflation remaining above the 2% target for roughly five years, as policy had previously moved well above neutral, allowing cuts while still maintaining a restrictive stance. However, with terminal pricing now drifting toward - or even below - the market-implied neutral rate, that cushion appears smaller.

If higher energy prices feed more persistently into consumer prices, markets may begin to anticipate that the Fed’s next move could even be a rate hike.

Insights

Escalating tensions in the Middle East have lifted energy prices, raising the risk that the disinflation trend stalls. While central banks typically look through energy shocks, markets are increasingly concerned about second-round effects through expectations, wages and broader production costs.

As a result, the policy reaction function appears to be shifting. Rather than easing policy as previously expected, markets have begun to reprice a tighter path, with peak policy rate expectations moving higher across several developed economies.

Insights

Markets have begun to reassess the policy outlook across Europe as rising energy prices and geopolitical tensions revive inflation risks. For the ECB, some policymakers have warned that a rate hike could come sooner than many expect if higher energy costs feed back into inflation

Meanwhile, expectations for further Bank of England easing have already been pushed back, with several institutions revising their outlook for additional rate cuts as the inflation outlook becomes more uncertain.

Insights

Energy shocks often coincide with a stronger dollar, as investors seek liquidity and safety in the world’s primary reserve currency during periods of geopolitical stress. The current conflict around Iran has already triggered a renewed safe-haven bid for the greenback alongside higher oil prices.

Historically, this combination tends to lead to a retraction in EM duration, as investors reduce exposure to longer-dated bonds and demand higher yields to compensate for tighter global liquidity, currency pressure and rising inflation risks.

Regionally, Mexico and Malaysia appear most sensitive to oil-dollar shocks, while Brazil and South Africa benefit more from dollar-liquidity regimes. Poland and Hungary show limited regime differentiation, reflecting stronger links to euro-area rates and deeper domestic investor bases that dampen external shocks.

Insights

Energy shocks typically reshape equity leadership through higher input costs, rising inflation risk and a widening equity risk premium. In this environment, investors tend to rotate toward defensive styles and larger companies, whose earnings are generally less sensitive to the macro backdrop.

Conversely, small caps and cyclical growth exposures often underperform. As a result, market leadership typically shifts toward value, high-dividend and defensive factors, while more cyclical style and size exposures tend to lag.