Fortnightly insights into what's moving the global markets.

This analysis dives into the latest U.S. bilateral trade data (UK having the only even trade balance)considering the impact of recent tariff announcements and the significant slowdown in key U.S. ports.

On the markets front, we assess asset performance (excluding the best and worst trading day) and highlight gold’s evolving positive correlation with real yields.

From a macroeconomic perspective, we observe global IMF GDP revisions trending downward (for all countries but three) and note how June's inflation uptick suggests Trump's tariffs are influencing key components.

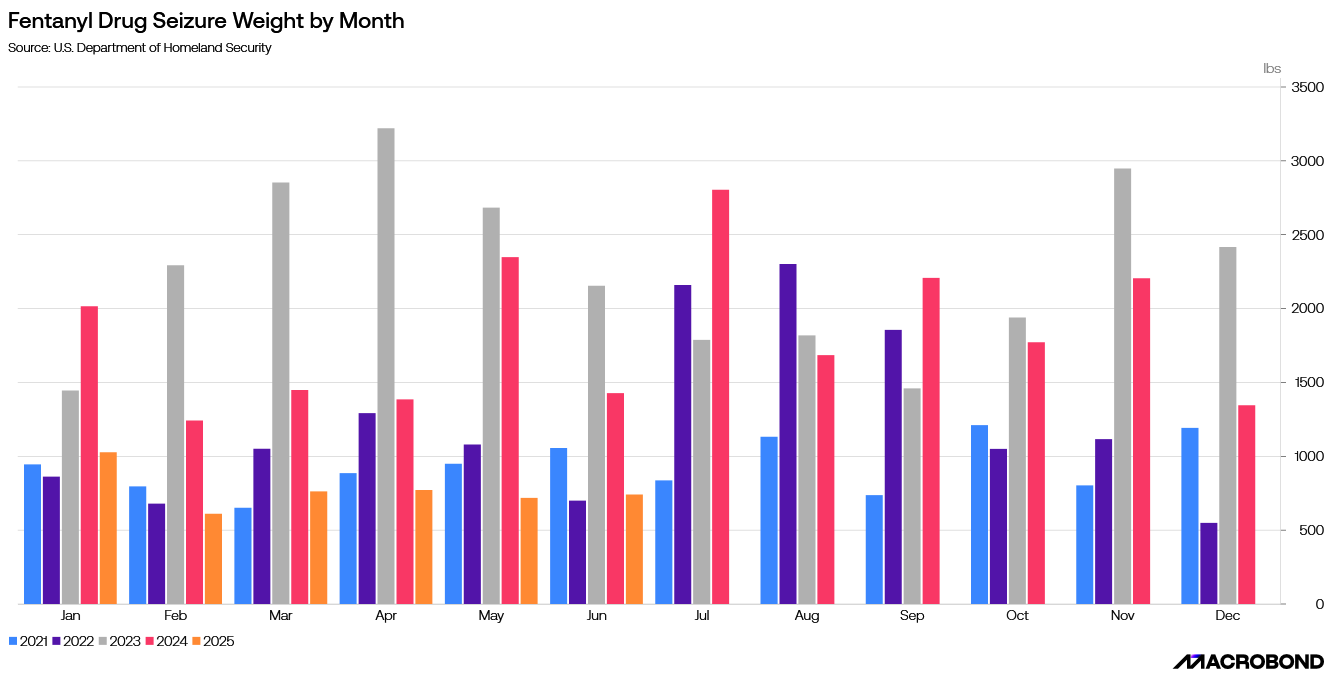

Lastly, we’ve added a chart on Fentanyl seizures through the years considering Trump’s initial tariff narrative.

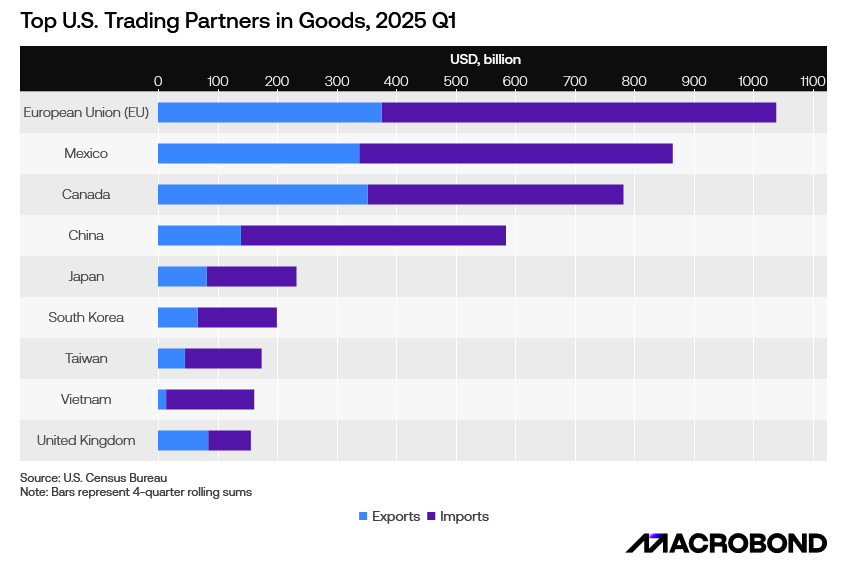

Trade flows between the U.S. and its major partners remain heavily concentrated among the European Union, Mexico, and Canada, each with annual goods trade above $700 billion.

Persistent trade imbalances, where imports far exceed exports, remains a central issue in U.S. trade policy debates, evidenced by President Trump threatening a 30% tariff on goods from the EU and Mexico effective August 1st.

Rolling 4-quarter totals highlight both the scale and trajectory of these trade flows heading into the upcoming tariff deadline.

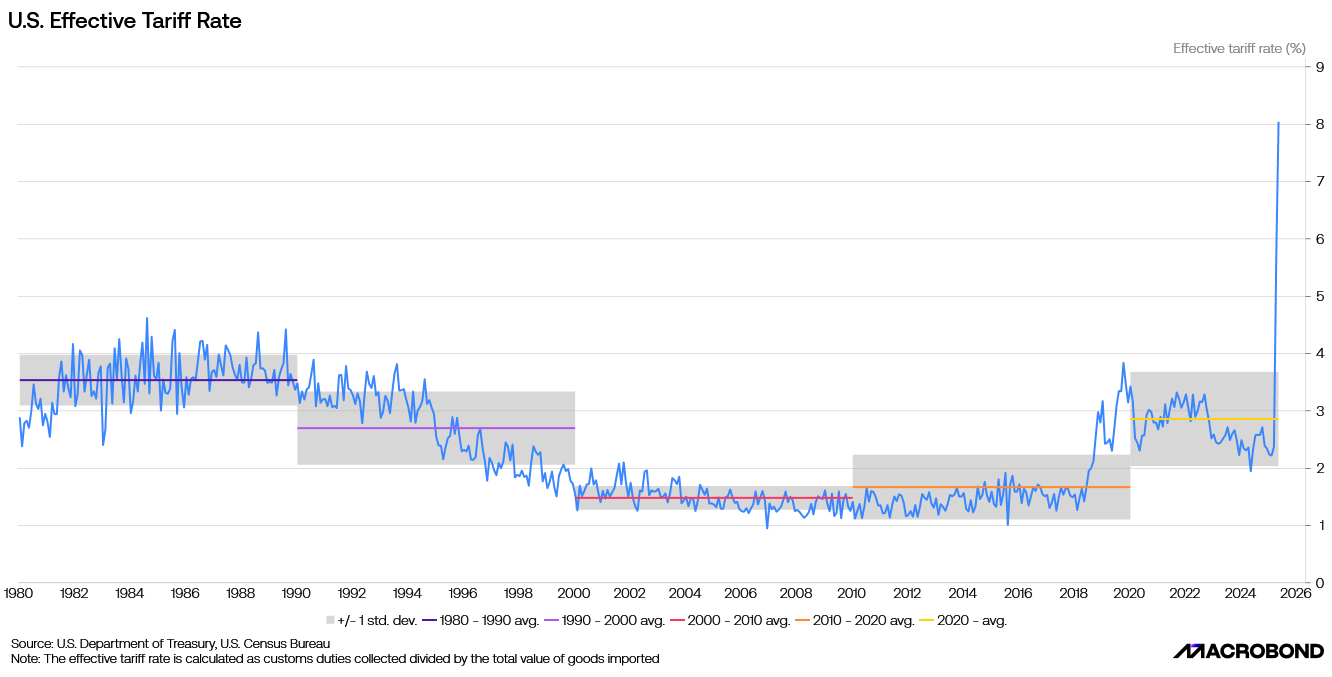

The effective tariff rate has surged, reversing decades of gradual decline that defined U.S. trade liberalisation.

While prior spikes, such as those during the U.S.–China trade tensions of 2018–2019, proved temporary, the recent increase appears larger and more abrupt. This suggests a decisive policy shift ahead of August 1, underscoring how current trade measures compare with historical trends.

.png)

Since Liberation Day, when tariffs were announced for most countries around the world, the Trump administration has announced several trade agreements, including with the UK, Vietnam, Indonesia, and just recently, Japan.

The most dramatic situation unfolded with China, as both the US and China escalated tensions by raising tariffs on each other throughout the spring. This tit-for-tat escalation eventually led to a preliminary agreement reached in May.

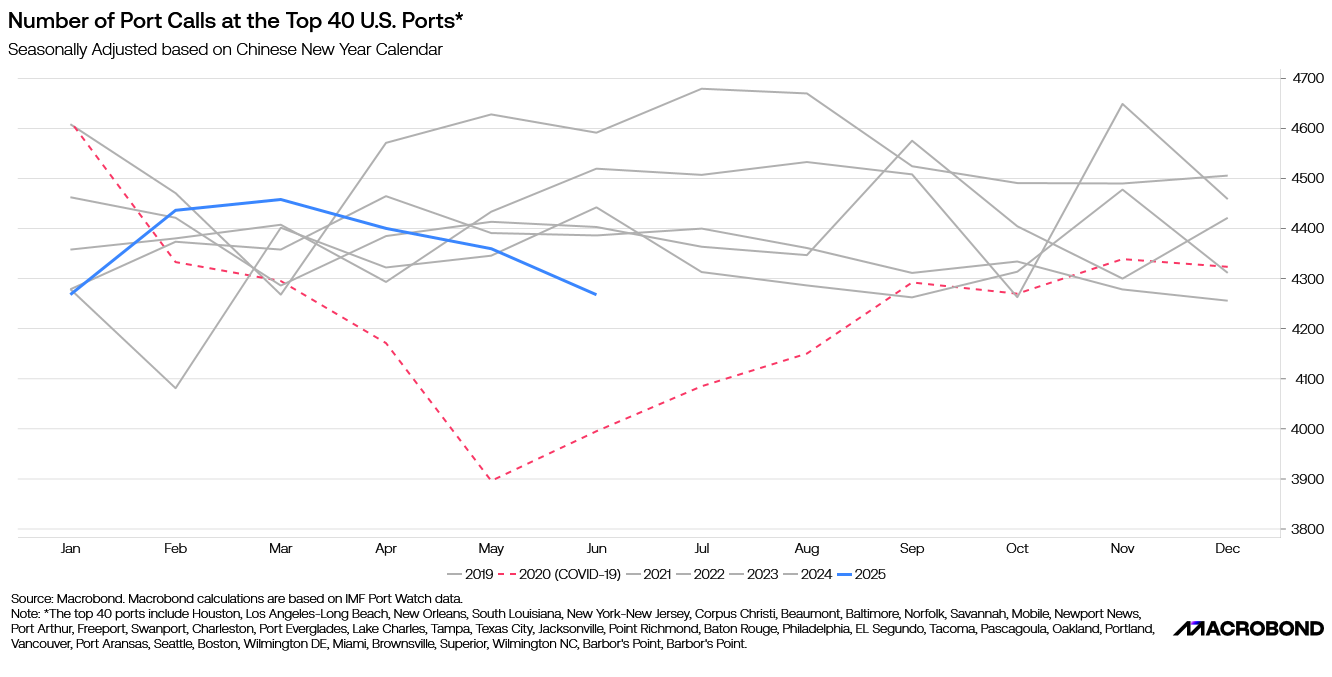

Port activity has slowed significantly, with the number of port calls at the top 40 U.S. ports reaching its lowest level as of June 2025, excluding the disruptions seen during the COVID-19 pandemic in 2020.

Seasonal trends are evident in the data, but the current decline appears sharper than in prior years. This may allude to softer trade flows in the lead-up to tariff changes and shifting global supply chain patterns.

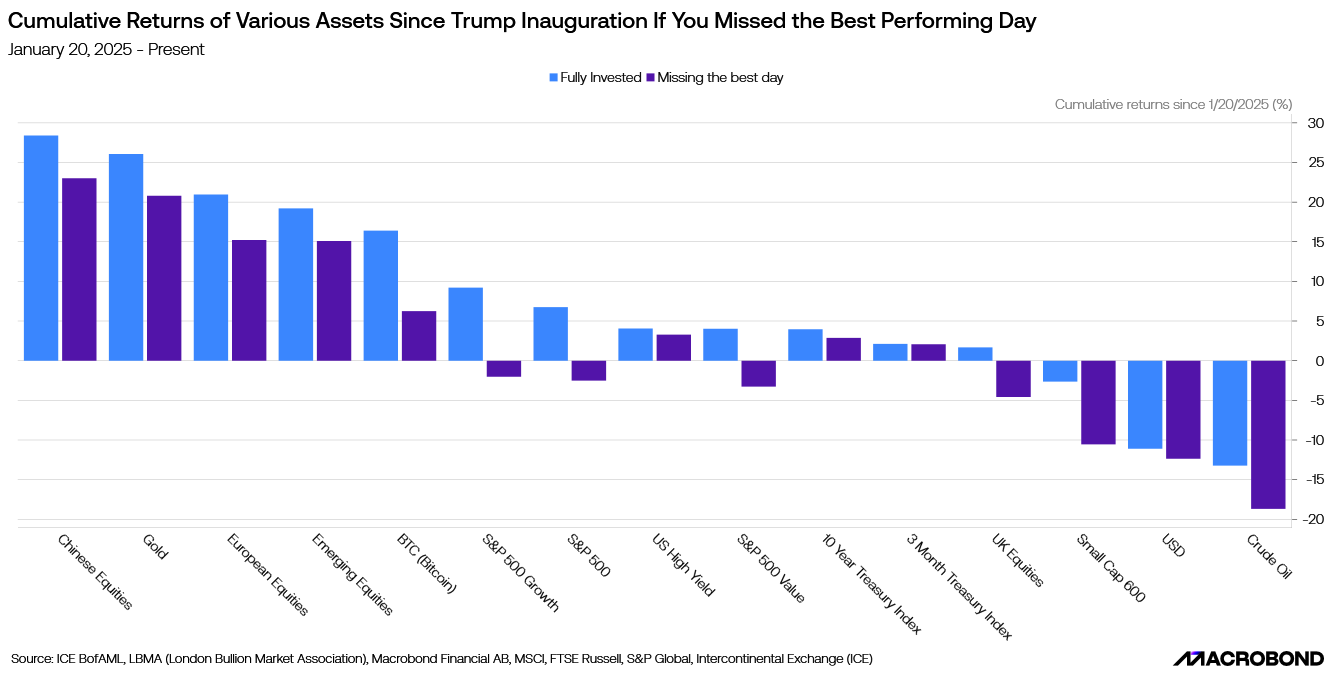

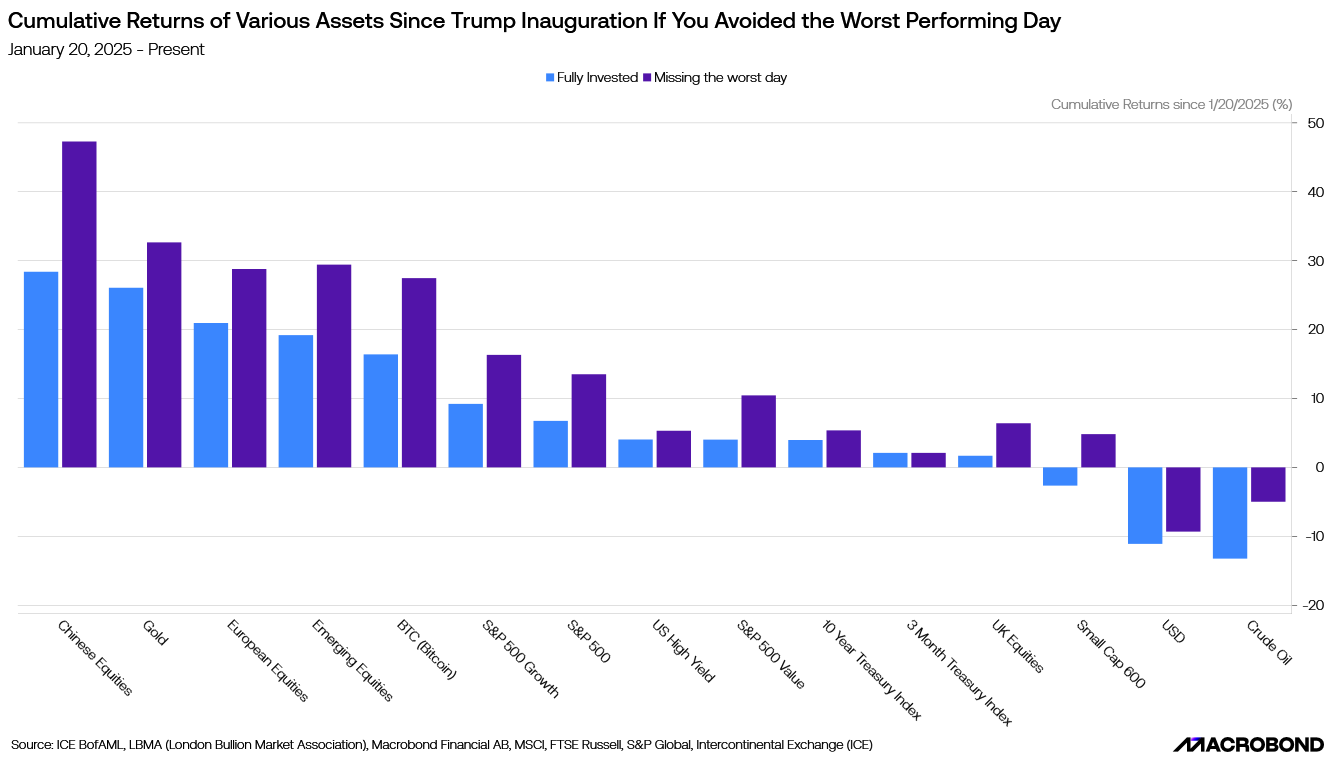

Market performance since Trump's inauguration has been uneven, a comparison between “fully invested” returns and returns excluding the single best-performing/worst-performing single day emphasizes how short bursts of gains/losses have driven cumulative performance.

In some instances, such as the S&P 500, missing just one of these standout daily returns would have turned overall performance on its head. This data shows heightened market sensitivity to policy developments and how short-term volatility can significantly impact returns.

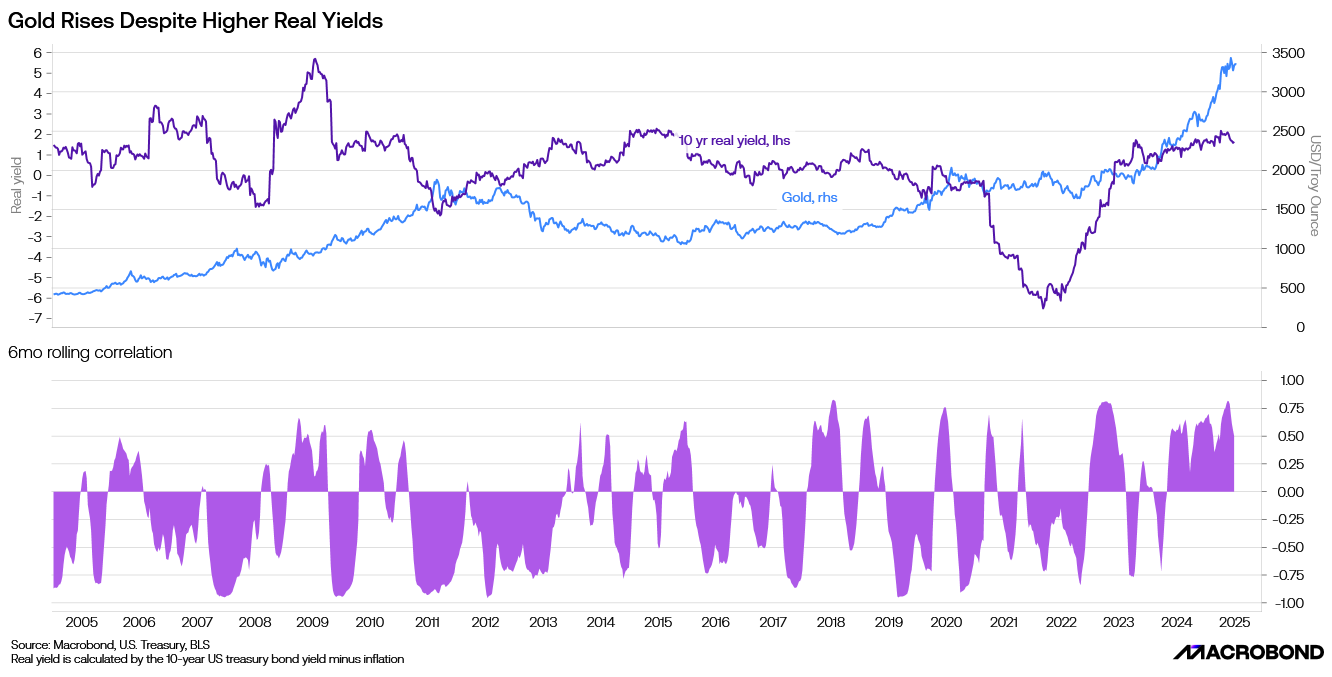

Historically, gold and real interest rates have mostly shared an inverse relationship with Gold rising when real yields fall, typically during times of elevated inflation. Despite occasional divergences, the six-month rolling correlation between the two has typically been negative. In recent months, however, it became positive for a sustained period.

Gold appears to be acting less as a hedge against inflation or interest rates, and more as a buffer against policy volatility and global disruption.

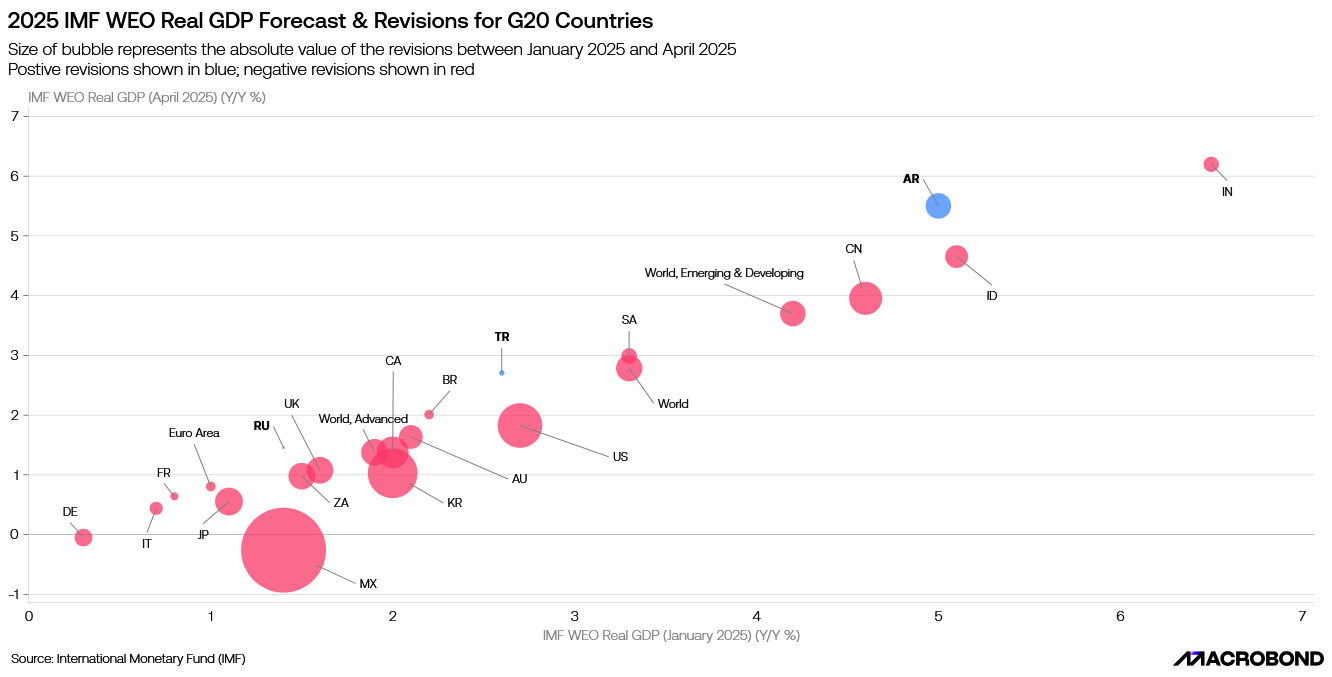

The IMF’s latest forecast updates highlight the economic strain created by the US’ unpredictable trade stance.

Between Jan and Apr ‘25, Mexico, South Korea, and the US saw the largest downward revisions to their ‘25 growth projections, indicating uncertainty around trade and investment.

In contrast, Argentina recorded the most significant upward revision, signaling improving expectations for its economic trajectory.

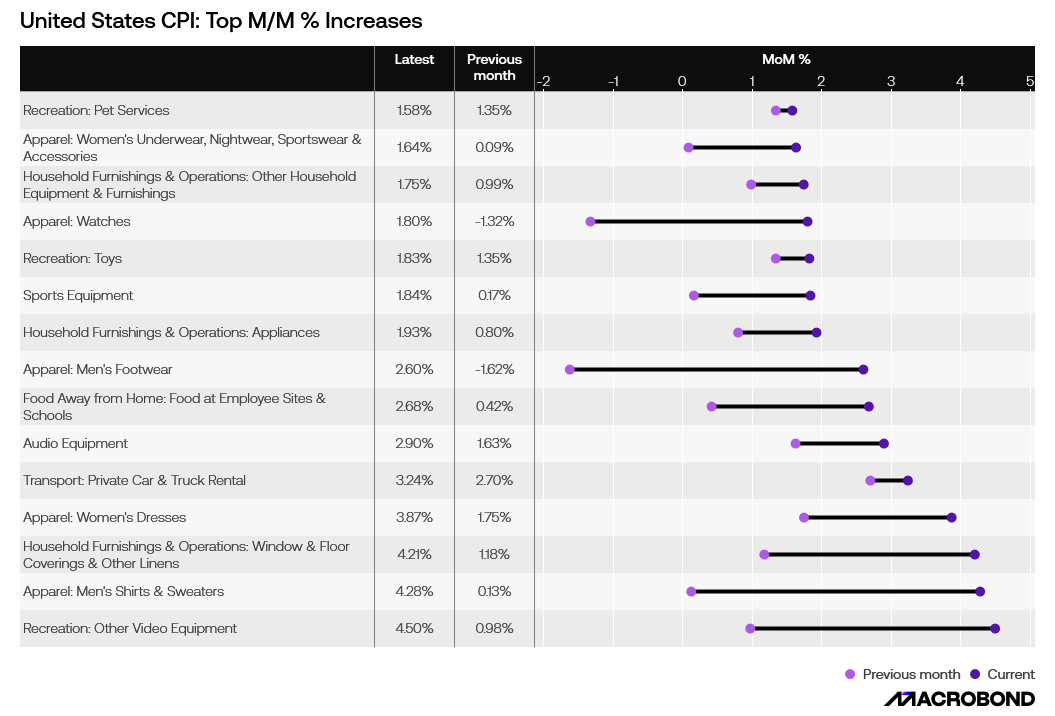

June inflation ticked higher (+2.9% MoM), suggesting that Trump's tariffs may be starting to impact consumer prices.

This chart highlights the 15 CPI components with the largest increases relative to May 2025, highlighting several tariff-sensitive categories with notable jumps.

Apparel saw some of the sharpest month-over-month increases, swinging from minimal or even negative changes in May to notable price hikes in June.

While some firms chose to stockpile inventory in anticipation of tariffs, other retailers appear to have begun passing higher costs on to consumers. July and August inflation prints will be critical for assessing how broad and persistent the tariff-related impact may become.

Trump has tied new tariff threats to the fentanyl crisis, citing it as a national emergency.

A 30% tariff on Mexican imports is set for August 1 unless Mexico escalates anti-drug efforts. China also faces renewed tariff pressure over its failure to curb exports of fentanyl’s underlying chemical exports.

The recent drop in seizures may reflect a temporary deterrent effect due to threats of stricter trade or border actions.