Fortnightly insights into what's moving the global markets.

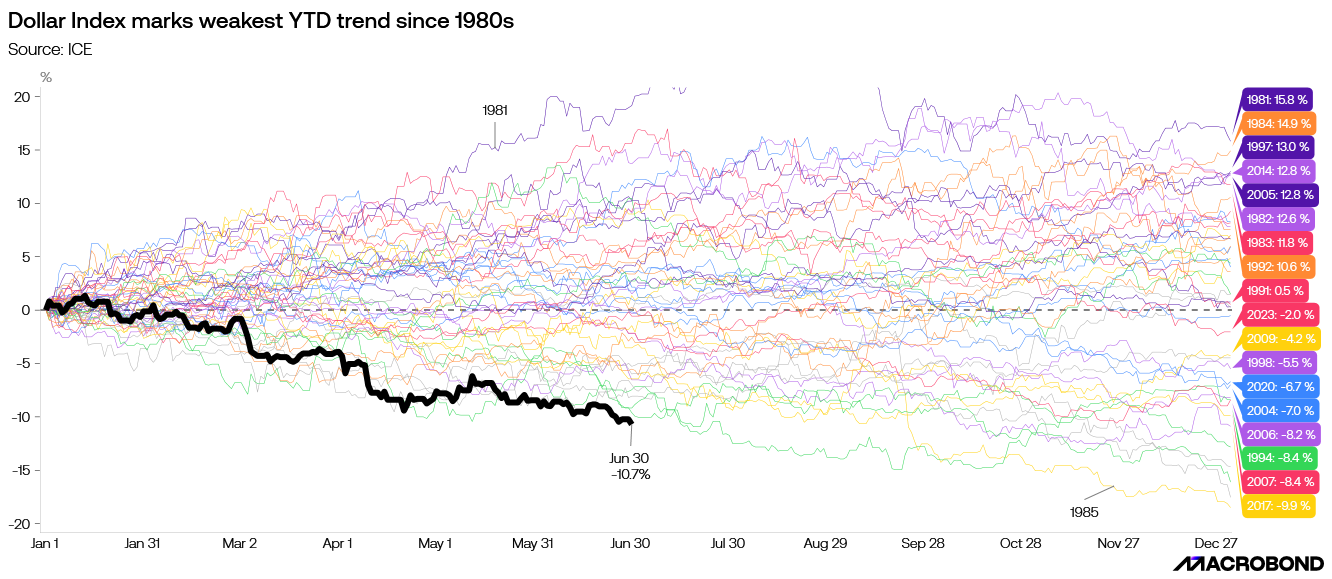

YTD Dollar depreciation breaches levels not seen since the 80’s.

We’ll start by looking at the main drivers behind the 10%+ Dollar decline we have seen this year:

1. Tariff turbulence

2. Fiscal and Debt concerns

3. Rate cut expectations

4. Heavy market positioning

Amidst these structural challenges, two recent tailwinds appeared to provide medium term support to the Dollar:

1. Section 899 (Revenge Tax) rescission from the One Big Beautiful Bill (OBBB)

2. Clearance of the GENIUS Act in the Senate (when passed ahead)

Sharp dollar declines were previously observed in the mid-1980s, driven by the Plaza Accord, Fed policy easing, coordinated international political action, and a valuation correction following strong appreciation.

In H1 2025, the USD faces downward pressure from various structural, economic, and policy-induced factors:

•Relative growth deceleration in the US.

•Rising fiscal challenges.

•Investment Shifts from portfolios increased exposure to non-US assets.

•Uncertainty around lower Dollar demand, likely tracking a probable lower US Current Account Deficit (CAD).

•Lower trade deficit, leading to less dollar recycling into dollar-denominated assets.

Citi Economic Surprise Indices are calculated as weighted historical standard deviations of data surprises relative to market expectations.

A positive reading suggests that economic releases have, on balance, been beating consensus.

For the US, the index swung to -8.7(Q2’25 avg) from a strong 22.1 (Q4’24 avg).

Comparatively, growth surprises have gone up nearly everywhere else globally bar LATAM, AUS, and CEE.

As tariff implications unfolded in H1 2025, economic effects on growth and inflation will emerge in stages.

Expect initial inflation pressure in H2 2025 due to direct tariff linkages, followed by a dip in consumption and investment. This environment will sustain policy uncertainty, affecting financial costs, liquidity, and exchange/interest rates.

Concurrently, stronger growth ex-US, especially in the stimulus-backed Euro Area, is shifting trade towards other currencies, adding further downward pressure on the USD.

With uncertain US policy this year, the above could come from investors having gradually added non-US assets, contributing to strength in non-US dollar currencies and weighing on Dollar.

The FCI-G* measures the cumulative impact of unanticipated, permanent changes in financial variables on real GDP growth over the subsequent year, weighted by impulse response coefficients.

Decomposition of the FCI-G (1-year look-back) reveals that the strong Dollar has posed headwinds to US GDP growth since 2024.

However, the aggregate FCI-G remains comfortably easier at -0.3, a more favorable position compared to the previous US recession's mean FCI-G of0.52.

Regression analysis of US GDP against the FCI-G indicates a marginal uptick in forecasted Q2 2025 GDP growth.

*Note: FCIs index aggregates changes in seven financial variables—the federal funds rate, the 10-year Treasury yield, the 30-year fixed mortgage rate, the triple-B corporate bond yield, the Dow Jones total stock market index, the Zillow house price index, and the nominal broad dollar index—using weights implied by the FRB/US model and other models in use at the Federal Reserve Board

A comprehensive array of financial and market indicators, including derived indices for political and economic stability, do not currently point towards anear-term recession.

Latest trends for these indicators are compared to their 3-month prior recession mean values.

While recession probabilities have remained elevated this year, other key metrics offer a more reassuring picture: Credit spreads remain relatively tight, and both Excess Bond Premiums and the Financial Stress Index are comparatively lower.

However, the Partisan Conflict Index and News Sentiment Index continue to reflect persistent uncertainty in policymaking and the broader economic outlook.

Note:

1. The Partisan Conflict Index tracks the degree of political disagreement among US politicians at the federal level.

2. Daily News Sentiment Index is a high frequency measure of economic sentiment based on lexical analysis of economics-related news articles

Macro and market factors, combined with persistent policy uncertainty, are weighing on the Dollar; with diverging US economic trends and weakening correlations.

While the Dollar has historically remained strong during periods of higher fiscal deficit and lower policy rates, "Trump 2.0" policies have challenged this structural resilience.

Heightened volatility during this period has further weakened traditional correlations and, consequently, while US yield levels, fiscal deficit-to-GDP ratios, and policy rates remain elevated, the Dollar Index has notably diverged, depreciating.

Section 899 ('Revenge Tax') in the OBBB posed a significant risk to the $33+ tn USD-denominated assets held by foreign investors ~ $13 tn indebt and $16+ tn inequity.

A punitive incremental tax (5% annually, capped at 20%) on passive income wouldhave driven rotation out of US and into non-US assets, further pressuring theDollar.

Since 2021, foreign investors have already shown a passive move from long-term into short-term US debt holdings, 52.4% in 2021 > 55.7% in 2024.

Additionally, a larger percentage of equity holdings, 40% in 2020 > 55% in 2024, being more volatile and driven by alpha generation, could further weigh on the Dollar with the unwinding of aggressive positions.

…thankfully for the Dollar, Section 899 was removed from the OBBB on June 28th,following a G7 understanding, significantly reducing sell-off concerns for US assets.

Key US trade partners have strategically reduced their holdings of US securities, lessening their dependency on the Dollar.

For instance, China's US securities holdings in 2024 stood at approximately 4.5%,significantly lower than its pre-trade war holding of 9.5% at the end of 2016.

However, amidst tariff uncertainties in 2025, the US has announced significant new trade deals, including the US–UK Economic Prosperity Deal, the US-China Trade Framework, and a US-Vietnam Tariff deal.

These US trade deals can support the Dollar by:

•Driving demand for USD in global trade.

•Attracting foreign investment into US assets.

•Reinforcing its reserve currency dominance.

The US Senate passed the GENIUS Act by a vote of 68-30 on June 17th,strengthening prospects of the digital Dollar era and global Dollar dominance.

By mandating a 1:1 reserve backing of US dollars or very liquid US Treasuries for every stablecoin issued, the GENIUS Act enhances consumer confidence in stablecoins and increases demand of US backed assets.

Blackrock's launch of its first tokenized fund (BUIDL) in 2024 has, in no time, garnered $2.8 bn.

As the stablecoin ecosystem grows - potentially doubling from around ~$250 bn (already 1% of US M2 supply) to $500 bn by 2026 - it unlocks massive new demand for US government debt

The Act strengthens US’s global competitiveness against China’s digital yuan or EU’s MiCA compliant tokens.

The global crypto market cap is $3.3tn, ~9%+ of US nominal GDP.

Rising crypto prices, higher turnover volumes, and significant market cap have made blockchains an integral part of the financial system.

Trump’s recent comment “Bitcoin takes a lot of pressure of the Dollar” suggests reframing crypto as a strategic asset and hints at political cover for supportive legislation like the GENIUS Act, positioning it as part of a broader strategy to fortify the dollar in the digital age.

The GENIUS Act enhances regulatory clarity and opens the door for institutions -banks, custodians, and payment processors - to integrate stablecoins into infrastructure and payment rails.

This fosters safer, blockchain-based financial systems

Stablecoin clarity acts as a foundation, encouraging innovation in decentralised finance (DeFi) and digital asset markets.

This could help launch compliant, tokenized financial products across Ethereum, Bitcoin L2s, and beyond.